The Executive Delusion Oscillator

A behavioural model of executive perception

Anyone who has spent time building a company eventually encounters a curious phenomenon that does not appear in most business textbooks. It is not a financial metric or an operational KPI. It is better understood as an empirically characterized psychological instrument. I call this phenomenon the Executive Delusion Oscillator. Despite its widespread observability and measurable consequences, it remains absent from most business school curricula.

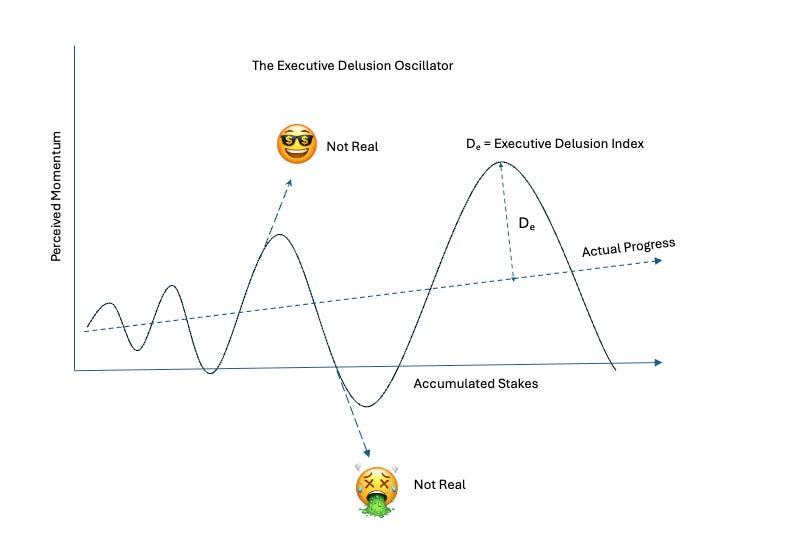

Reality in a growing company tends to move in a rather unremarkable way. Progress is uneven but generally upward. Problems appear, are addressed, and eventually resolved. If plotted on a chart, reality would look like a modest to decent rising line.

Perception behaves differently.

Perception oscillates around reality. At one moment the company appears destined for inevitable success. Shortly thereafter the very same set of facts suggests looming catastrophe. These swings rarely correspond to meaningful changes in the underlying trajectory. They are interpretations, often emotional, applied to incomplete information.

Early in a company’s life the oscillations are small and fast. A promising conversation may produce a burst of confidence that lasts an afternoon. A difficult meeting may produce the opposite reaction before dinner. Fortunately the stakes remain modest and the consequences of misinterpretation are contained.

As the company grows, something interesting happens.

Capital accumulates, expectations rise, careers, reputations, and investor capital become tied to the outcome. At this stage the amplitude of the oscillations begins to increase dramatically. A small positive signal becomes evidence that unstoppable success is now inevitable. Leadership metaphorically puts on sunglasses and begins counting money that has not yet arrived. The opposite swing is equally familiar. A setback produces existential dread and the entire enterprise suddenly appears doomed. Emergency strategy meetings appear, investors begin to bristle, and the CFO quietly begins documenting that this was not their idea.

Neither conclusion is usually correct.

Reality continues along its slow and stubborn path while perception swings wildly above and below it. Empirically, oscillation amplitude can be described as the Executive Delusion Index (Dₑ), though measurement techniques remain unreliable.

Integrating the oscillator across time yields the Cumulative Delusion Load (CDL), a quantity that appears strongly correlated with emergency strategy meetings, late night Slack threads, and the quiet creation of a new “scenario analysis” tab in the financial model:

CDL(T) = ∫₀ᵀ |Dₑ(t)| dt

where

Dₑ(t) = Executive Delusion Index at time t

T = total time horizon of the venturesince

CDL = ∫₀ᵀ |P(t) − R(t)| dt

where

P(t) = perceived momentum

R(t) = actual progressInterpretation:

CDL represents the Cumulative Delusion Load, defined as the total organizational load generated by the integrated divergence between fantasy and reality over the life of the venture. Or more simply:

CDL ≈ Total accumulated executive wrongness.

It is further observed that

CDL(t) ∝ Dₑ(t)² for t ∈ F

where F represents intervals coincident with late-stage funding rounds. Empirical measurement remains confounded by optimism bias.

Finally, we define the Point of Maximum Delusion, PMD, as the time t* within F at which executive delusion reaches a local maximum.

Formally,

t* = arg max Dₑ(t), for t ∈ F

A necessary condition is

dDₑ(t)/dt |_(t=t*) = 0

and a sufficient second order condition for a local maximum is

d²Dₑ(t)/dt² |_(t=t*) < 0

Therefore, the Point of Maximum Delusion occurs at the critical point during the funding interval where the Executive Delusion Index ceases increasing and begins to decline.

Equivalently,

PMD = Dₑ(t*) = max {Dₑ(t) : t ∈ F}

Interpretation

The PMD represents the moment during at which executive perception is most completely decoupled from reality.

Operationally, this is often observed shortly after the largest valuation number is spoken aloud, but before any corresponding operational miracle has taken place.

Common empirical indicators include:

• the phrase “this changes everything”

• headcount plans that assume frictionless execution

• references to inevitable category leadership

• investors suddenly becoming “strategic”

• a CFO opening a new tab titled scenario upside

Informally

PMD ≈ the precise moment everyone starts acting as though the money has already turned into success.

Experienced operators eventually learn to recognize the pattern. The peaks are rarely as real as they feel, and the troughs rarely represent the end of the story. The task is not to eliminate the oscillator, which appears to be a permanent feature of ambitious undertakings, but to avoid steering the company based on its most dramatic swings. In practice, progress tends to occur somewhere near the middle line, where the story is less exciting but considerably more accurate.

"They are interpretations, often emotional, applied to incomplete information." This line says it all. A fun and emotionally accurate ride on the roller coaster!